Disclaimer: THIS POST IS NOT FINANCIAL OR INVESTING ADVICE. If you’re looking for that, consult with someone working as a financial advisor and/or (maybe not) the Twitter/Reddit stonk memes.

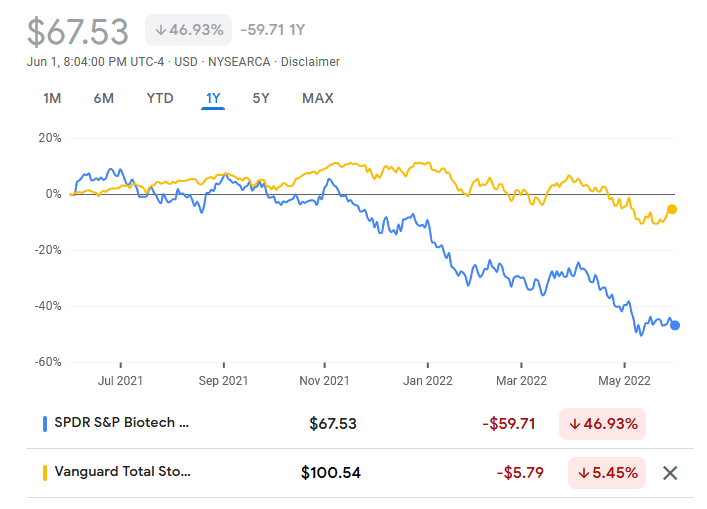

Public biotech valuations have collapsed, plummeting far beyond the overall market. Much has been written about public biotech bust (here, here, here, and Google if you want more….) Ideas on why it’s happening range from too many pre-clinical companies, too much capital, too many companies, a comedown after the rush of the pandemic, and plain old investor sheep behavior. It could, and probably is, a little of all of the above.

How does this impact biotech startups and private biotech? My instinct is that it’s a bad sign for the private market as well, primarily for late-stage companies. The public market represents one of the two successful exit pathways for startups. Private investors (e.g., venture capital, private equity) get their money back, ideally many times over, when a startup gets acquired or it IPOs. With biotech valuations this low, startups will hesitate to go the IPO route because they won’t be able to raise as much money, or perhaps even enough money to keep going. At these values private investors also won’t make back much of a multiple, or may not even make back the money the put in.

There’s a double whammy here too: cut off the IPO path and what’s left is acquisition. While there are multiple pharmaceutical companies that could acquire startups, there are relatively few (maybe 20-50 companies) compared to the thousands of biotech startups in the U.S. alone. Pharma companies do a limited number of acquisitions each year and a few have indicated they think acquisition prices are still too high. Knowing IPOs aren’t an option, pharma companies can wait until prices drop to a bargain. Again, private investors and founders lose money. At some point acquisition could increase enough to cover the volume of companies that would instead IPO, but that won’t be immediate.

Earlier-stage companies raising Seed and Series A are a bit safer for now, but it will get more challenging the longer this drags on to months or years. They’ll find it harder to raise Series A, Series B or subsequent funding as venture capital firms save funding to help the startups they’ve already invested in weather the storm and wait for better offers from IPOs or pharma acquisitions. There may also be less funding overall available, as private investors see poorer returns from biotech and allocate their money elsewhere.

What would turn this around?

First, there are larger trends that are weighing down the market overall: Fed tightening to reign in inflation, the war in Ukraine and the impact that has had on oil prices, and COVID-related supply chain disruptions are issues (quick explainer here at Reuters). If any or all (ha) of these were to disappear, we would likely see a rebound in the entire market, including some in biotech. But it probably wouldn’t be enough.

Ultimately what we’d need to see are one of two things:

- Signs of clinical and commercial success from public biotech companies. Remember, these companies are all operating at a loss (and often with little to no revenue) until they have an FDA-approved and marketed therapy. A few success stories just making the leap from no product-based revenue to a quarterly revenue stream that meets or exceed projections would be good news.

- Increased appetite for acquisition from pharma companies for private biotech companies at valuations that allow private investors to make a multiple on their invested funds. This would provide an alternative exit to an IPO that would keep funds going and private investors focused on biotech.

Will this happen. Who knows?